One of the most anticipated IPOs of 2014 is just about to happen, the going public of the Chinese Internet company Alibaba Group. This may be the biggest US IPO ever with the float approaching USD20 bn, surpassing even Facebook’s IPO. There’s a view out there that the IPO may happen on August 8 as eight is a lucky number in China but a date after Labor Day when investors are back from summer vacations seems more likely.

In the tale of “Ali Baba and the Forty Thieves”(from “One Thousand and One Nights”) the poor wood cutter Ali Baba gets access to the den of the thieves by saying “Open Simsim”. The secret door opens and the treasures of the thieves lay ahead of him. Expecting to find a dark, dismal cavern, Ali is surprised to see a spacious chamber full of light and filled with all sorts of provisions, rich bales of silk, embroideries, and valuable tissues, gold and silver ingots in great heaps, and money in bags. Less well known is that the brother of Ali Baba, described as the greedy Cassim, was killed in an attempt to collect some of those riches as he forgot to use the magic word to leave the den and was seized by the thieves.

So, the obvious question for us is whether investors in the Alibaba Group will have access to yet to be valued treasures or will they get caught up badly in the process of investing?

While we do not have the final answer, we want to lay out some facts on the company. Alibaba Group was founded 15 years ago by 18 people led by Jack Ma, a former English teacher from Hangzhou, China. By 2013, Alibaba accounted for 80 % of all ecommerce in China, already the largest internet market globally in terms of users. As internet penetration in China has only reached 50 % so far- well below the 80 % level in countries such as the US - China clearly will become an even much bigger market going forward, potentially even the largest ecommerce market by 2025.

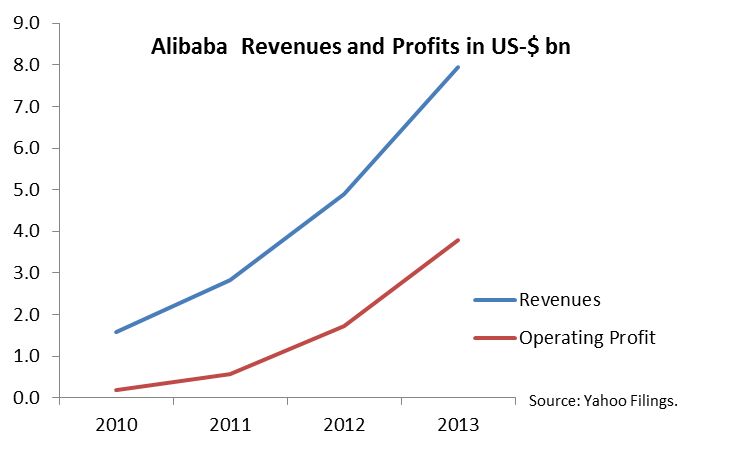

The two key pillars for Alibaba are Taobao, a marketplace mostly for smaller businesses offering products to consumers, and the even faster growing Tmall, a type of shopping mall for larger sellers and brands. The company earns money by a mix of advertising on those sites and a slice of the value of the goods traded there. Over the last twelve months more than USD250 bn of merchandise changed hands through those two channels, generating roughly USD9 bn in revenues for the company. Taobao and Tmall are only active in China but Alibaba has also started to ramp its businesses internationally. Furthermore in the last 12 months it has acquired a long list of companies, from logistics to online video, in an apparent preparation of a broader service offering. Overall top line growth in 2013 had been an amazing 62 %.

Alibaba is highly profitable and achieved net margins of 45% last year as (in contrast to Amazon) they do not hold any inventory.

With all of that positive news, where are potential issues?

First of all, from a corporate governance perspective, as a minimum investors need to be aware of the following issues: A partnership of certain executives including Jack Ma is exclusively allowed to nominate a majority of Alibaba’s board. Furthermore, like many Chinese companies, Alibaba uses a legal structure known as a variable interest entity (VIE), to get around Chinese government restrictions. Next, in 2007 the group listed its business directory subsidiary under the name alibaba.com in Hong Kong (Ticker 1688 HK), a less successful episode which only ended with going private into the arms of the group company in 2012.

Financially, the biggest question is if those extraordinary margins are really sustainable. EBAY has net margins of less than 20 %, Amazon less than 2 % and Google of 22 %. Hong Kong-listed Tencent, the company behind the Wechat network in China, is running at a bit above 25 % net margins. Jack Ma had made already clear that Tencent is one of his targets to beat, implying significant investments to compete.

Some of the assets of the Alibaba group will not be part of the flotation including both the payment business Alipay and money market fund Yu’e Bao which has seen phenomenal growth.

While China is a huge market, the transition to mobile is still in its early days and Alibaba’s growth slowed significantly to 42 % in Q1 as monetization on a mobile is below that on a PC. Google underwent the same experience in the last two years and we expect Alibaba’s growth rates to stay under pressure for a similar time period. Mobile accounted for only a quarter of the value of all goods traded on Alibaba in the first three months of 2014.

Finally, the question which is really on the mind of all investors at the moment is how much is Alibaba worth. Some analysts working for banks not involved in the IPO have issued estimates for Alibaba. Net income is estimated to more than double from last year’s level USD3.6 bn to close to USD9 bn in 2017. Given predicted earnings growth of more than 30% p.a. for the years 2015-2017, it is not unreasonable in our view to assume the stock is trading at a 30 multiple off 2017 earnings. Discounting this back two years with 15% p.a. gives an implied fair value of USD190 bn. On this, we would also put a discount of around 10-15%, for the corporate governance issues mentioned above, leading to a revised value of USD170 bn. With a typical IPO discount of 10% and based on the analysis above combined with the research that has been published by various banks analysts we would not be surprised if the banks leading the IPO were to value Alibaba at circa $150 bn.This assumes that the margins are sustainable and the execution indeed lets the company grow along the estimates mentioned.