Currencies tend to show up on the front pages only when they are in turmoil, which feeds perennial suspicion and contributes to many investors avoiding the asset class altogether.

As someone who has been managing currencies for 28 years, I have seen this concern ingrained in the market's conventional wisdom. This leads to the investment arena being underused and underappreciated, which comes at a cost to the investment community.

All this time that investors have been seeking new sources of return, diversification, and markets, currencies have always been here, providing these benefits for investors who know where and how to look.

There are multiple reasons why currencies can be a robust and legitimate source of excess returns. Two of the most compelling ones are: 1) currencies revert to their fundamental values, often faster than equities or bonds, which creates exploitable opportunities; and 2) the carry trade can be a powerful opportunity for investors to make money.

Despite being a “scary” currency that people hear about only when it's having some large negative move, the Russian ruble over the past several decades illustrates both of these characteristics.

Ruble Reversion

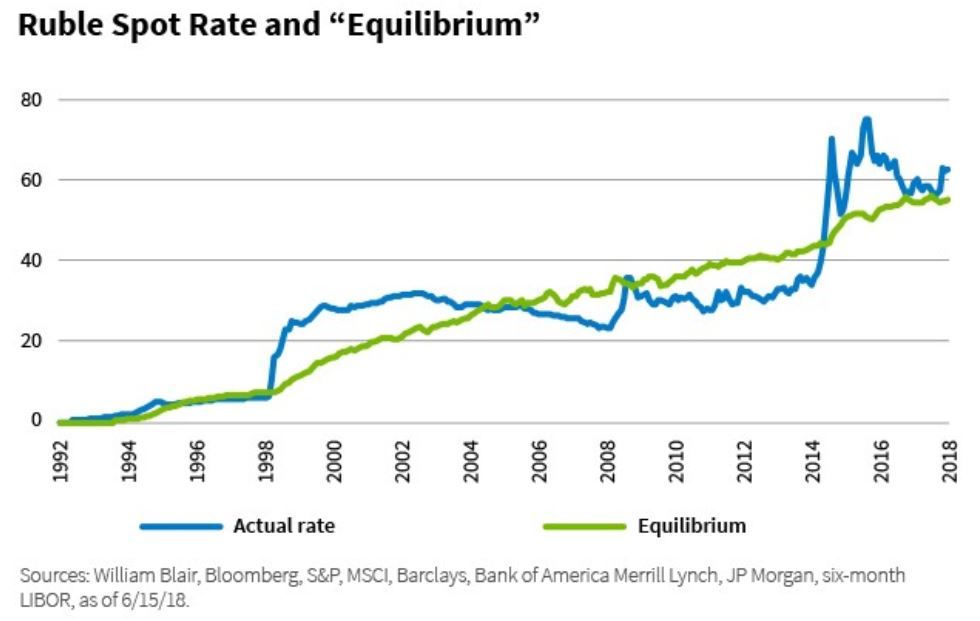

The chart below shows the Russian ruble relative to the U.S. dollar. The dark blue line is the actual exchange rate and the green is the equilibrium rate the ruble would take if its price relative to the dollar was affected only by changes in Russian inflation relative to the U.S.

That is, both the actual exchange rate and the equilibrium exchange rate are in nominal (money) terms, which are the terms on which we trade currencies in the real world. As you can see, the ruble appears to be on an ever-weakening trend against the dollar since the end of the Cold War.

Also, if you just look at the actual rate in isolation, the ruble looks like many “scary” emerging market currencies, with periods of relative stability followed by huge spikes upward—essentially a bumpy, unpredictable trip “to the moon with no return to Earth.”

But the proper way to evaluate any currency is through the lens of its fundamental, or equilibrium, value. When you plot the nominal rate against the equilibrium rate, you see that over the past 20 years, the ruble has had two significant periods of being overvalued and two significant periods of being undervalued.

These overvaluations and undervaluations are what provide the opportunities to benefit. Using this sample, the ruble reverts back to its sustainable equilibrium rate every 5 years, which means that an investor, at a randomly sampled point in time in the history, would have to wait an average of 2.5 years for the currency to revert to its equilibrium.

This may not seem especially fast, but it's important to note that it's significantly faster than what you see with most equity markets. It's an opportunity investors can take advantage of, particularly if the ruble is part of a broad universe of currencies in a portfolio.

We can invest, for example, in more than 30 currencies around the globe.

Carrying Its Weight

But returning to the chart above, the ruble has been getting weaker in nominal terms, and so has its sustainable equilibrium. Each time the lines converge, it is at a weaker ruble exchange rate to the U.S. dollar than the previous time that a mis-valuation was corrected.

Many investors interpret these lines as showing that money cannot be made from being long (overweight) or rubles. After all, how can one make profits from being long of an undervalued ruble if the correction of this undervaluation occurs at a weaker ruble than last time, and probably at a weaker ruble level than at which the position was bought?

The reality, however, is that the lines on the above chart exclude relative interest rate gain or loss (carry). With almost all tradable currencies, nominal interest rates at least compensate for inflation over time.

The ruble persistently weakens in nominal terms (excluding carry), and this is justified because Russian inflation was persistently higher than U.S inflation (“justified” refers to the observation that the equilibrium ruble rate weakens just as the actual rate does, although in a less volatile fashion).

To wit, if the carry is included, which it is when we trade currencies in the real world, then it is possible to make money by being long of high inflation and undervalued currencies, even if they persistently depreciate through time.

What appears to be a cumulative weakening trend for the exchange rate does not mean cumulative negative total returns from holding a position in the currency.

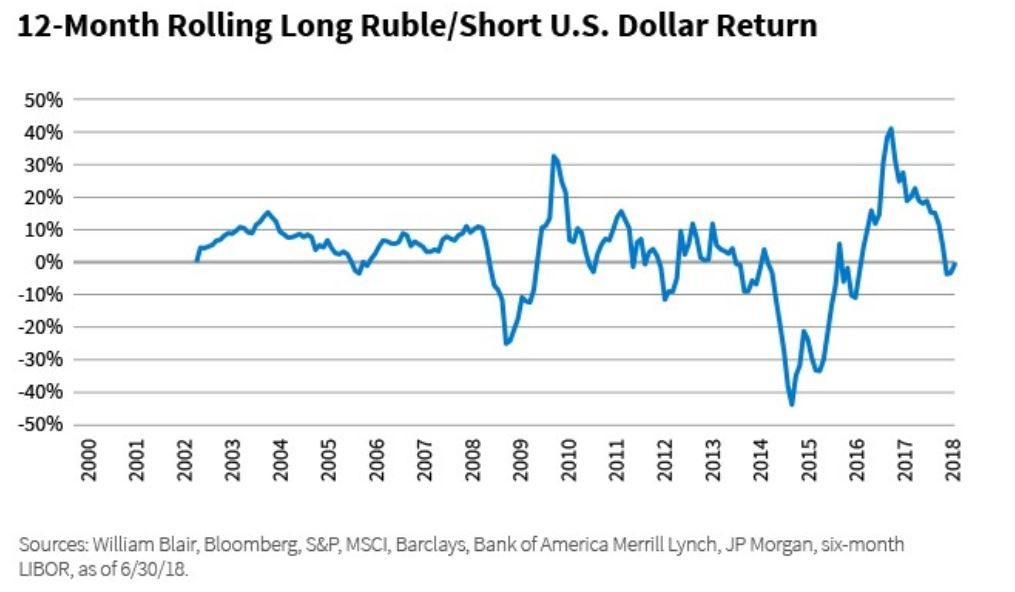

The chart below shows the 12-month rolling total returns from exchange rate and relative interest rate carry that an investor would get from a passive “buy-and-hold-forever position” that was long rubles and short dollars.

Note that this return series, unlike the exchange rate graph, is not a cumulative weakening trend. In fact, the cumulative return over this period is positive. Over the long term, the ruble has actually outperformed the dollar on a passive “buy-and-hold-forever” basis when measuring total returns exchange rate plus carry. This is the case even though the ruble exchange rate to the dollar has persistently weakened.

It's not a one-way losing trade. This is the case for just about every currency one can trade.

Actively Pursuing Opportunities

Of course, as active managers, we aren't taking a passive buy-and-hold-forever approach to any of the currencies we manage. We are looking to avoid some of the rolling negative return seen in the previous chart and capture more of the rolling positive return by using an active approach that is anchored in fundamental value.

Essentially, when the ruble was undervalued, then we would want long ruble exposure, but when it was overvalued, we would not, and we would prefer short exposure.

Even more specifically, we are looking for signals that indicate when the gaps between price and fundamental value are going to widen or narrow.

Often these signals involve evaluating the differences between current currency prices and fundamental value in different risk environments or by analyzing how nonfundamental (e.g., geopolitical) influences may cause prices to move further from, or closer to, value.

In any asset class, active investors have the ability to beat passive strategies because gaps between price and fundamental value are ultimately corrected. They open, they close, and they generate excess return opportunities along the way. With currencies—even “scary” ones such as the ruble—investors often don't have to wait too long for that to happen.

Tom Clarke

Portfolio Manager

William Blair Investment Management

Tipp: Dieser Beitrag ist auch im "Investment Insights"-Blog von William Blair verfügbar.

William Blair Updates per E-Mail erhalten