Overview of the asset class

e-fundresearch.com: Opportunities in high yield: What makes the global high-yield asset class an attractive long-term investment? Steve Logan: Since 1987, the high yield sector has generally produced healthy risk-adjusted returns, striking a good balance between return and risk. With almost 30 years of proof of concept, the US high yield sector (as represented by the BofA Merrill Lynch US High Yield Constrained Index) has provided over 80% of the upside and less than 60% of the downside when compared to equities (as represented by the S&P 500 Index). As such, high yield remains a strong diversifier within an investor’s portfolio for those who can tolerate the risk.When we consider the expanded opportunity set in the global high-yield market, we think an investor can gain considerable advantages. These include:

- Diversification into non-US securities. This could reduce a portfolio’s overall risk, as these securities have historically shown lower correlations to domestic securities.

- Focus on global industry leaders. For example, a leading commodity producer might be located in South America, while a leading technology or service company might be located in the US or Europe.

- Exposure to a more favourable investment environment due to variances in the global monetary policy cycle.

- Differences among global regulatory environments. Regulations that may present challenges for an industry in the US could favour the same industry outside the country.

- Potential for increased liquidity. During periods of domestic market stress, foreign high-yield markets may provide more liquidity than the US Liquidity during down markets is often considered the “Achilles heel” of the high-yield asset class, and investing abroad may help address this weakness.

Over the last 10 years, global high yield bonds have outperformed other fixed income asset classes. Global High yield has outperformed the investment grade universe as represented by the Barclays US aggregate by 3.1%. Within the corporate segment of the investment grade universe, global high yield has outperformed by 2.0%.

Impact of recent market events on the asset class

e-fundresearch.com: What do you think will be the impact of a potential US rate hike on high yield bonds?

Steve Logan: While a hike from the US Federal Reserve (Fed) appears imminent, we do not believe that this undermines the investment case for the high yield asset class. While the short end of the yield curve will see pressure, we believe that the intermediate and long-term yields will be mainly be driven by inflation expectations and, in an income-starved world, the continued search for yield.

Following the Donald Trump presidential election victory, inflation expectations soared. The credit spread on longer dated maturity high yield bonds managed to absorb much of the yield shift, and this helped high yield to outperform lower yielding and longer duration US Treasuries and investment grade credit. By its very nature, high yield is a short duration asset class and benefits from the ability to re-price relatively easy without causing large capital losses.

The high coupons and short duration are a powerful combination. The major risk is from defaults – not recent rates. Rising rates typically signal a healthy economy, which is an environment that can benefit high yield companies.

e-fundresearch.com: Are you concerned with default activity going forward?

Steve Logan: Global default activity, while higher than year-ago levels at 4.7%, have generally been consistent with expectations and almost exclusively contained in the commodity related sectors. With the roll-off of defaults from early in the commodity bust and the recent bounce in commodity prices, we believe that we have passed peak default levels for the year as we enter the fourth quarter. Despite the substantial spread tightening thus far in 2016, option-adjusted spread (OAS) levels over comparable duration government securities of 485 basis points (bps) as of the end of the October suggest that the market is still pricing in approximately 7% defaults over the next 12 months (assuming a 30% recovery rate), well above current levels.

e-fundresearch.com: How are you positioning the fund amidst global political risks?

Steve Logan: The path of most policies under President Elect Trump are still unclear. The initial market consensus; however, is that he will pursue a policy of fiscal expansion, stimulating the economy through a drive to renew old infrastructure and cutting the level of corporation tax. Bond markets reacted with the Treasury curve expressing a sharp bear steepening. We have a preference for shorter duration assets that should outperform in this environment. In terms of sectors, our healthcare bonds performed well given Trump is not expected to pursue the sector for aggressive pricing. On balance, fiscal expansion combined with a gradual path of hiking from the Fed is a reasonably supportive backdrop for the US high yield market. Emerging markets (EM) are suffering from dollar strength and longer dated assets have dramatically underperformed. We are positioned underweight EM debt but have made some opportunistic purchases recently. We are mindful of the volatile state of EM currently which could be exacerbated if sizeable global outflows are seen.

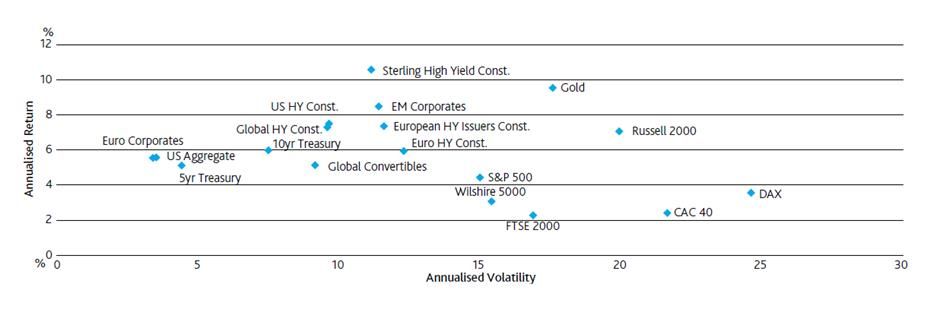

Historically attractive risk/return characteristics

e-fundresearch.com: What is your near-term outlook for global high yield bonds?

Steve Logan: As we survey the high-yield landscape, we remain cautiously optimistic about prospects for the asset class in the near to-intermediate term as we see pockets of both opportunity and risk to the asset class globally.

We think that the US high-yield market in particular presents both cautionary and bullish signals for investors. On the positive side, we see improving credit trends in the form of improving upgrade/ downgrade ratios. However, we see several factors that give us pause regarding the US high-yield market.

Most importantly, in our opinion, while we take comfort in the fact that the US economic recovery remains on track, we are cautioned by five straight quarters of earnings declines– predominantly in the energy space–and consensus forecasts for a sixth consecutive quarter for the reporting period beginning in October for the constituents of the S&P 500 Index.

The recovery, while ongoing, remains relatively weak, and the expansion is getting long in the tooth. While we see value in certain sectors of the US, we think that some caution is warranted, and credit selection will be the key to outperforming the market in coming months and quarters. Entering the fourth quarter, we saw a relatively more benign environment for high yield outside of the US, particularly in Europe. In several ways, we believe the European high yield market offers investors the mirror image of the US The economic recovery in Europe, while still fragile, remains in the early stages. Policymakers at the European Central Bank (ECB) continue to provide unprecedented levels of accommodation to the market in the form of bond purchases. The Bank of England has begun its own bond purchase program in an effort to head off any potentially pernicious impacts following the Brexit vote.

Both programs provide an underlying level of support for bond prices that is not replicated in the US market. Persistently low levels of inflation suggest that any hawkish policy actions are likely off the table for the immediate future—which we believe should benefit high-yield investors.

Taking these factors into account, we most likely will become increasingly selective in our credit selection process for companies domiciled or operating in the US, while placing additional emphasis on finding suitable opportunities in geographic regions such as Europe or the EM. In our view, such markets stand to benefit from improved macroeconomic backdrops.