e-fundresearch.com: Which benchmark do you adhere to and how important is the benchmark?

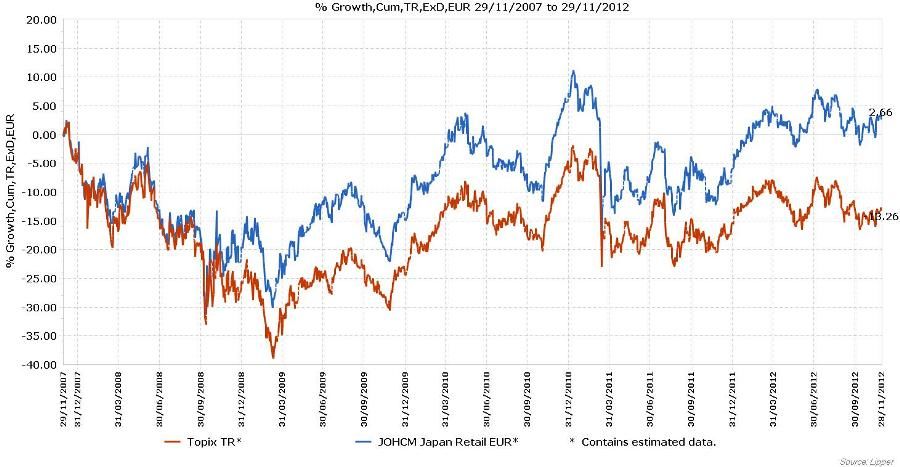

Ruth Nash: We manage the fund against the Topix Total Return Index, which we think is the most appropriate benchmark for the Japanese equity market. However, in building the portfolio we take little notice of the benchmark; it is more for performance comparison.

The primary investment area for the strategy is the TOPIX Mid 400 Index, the next largest 400 companies after the top 100. This is because the stocks in this index tend to be less well covered by sell-side analysts, but are still relatively large, liquid companies.

Ruth Nash: Our focus is solely on the Japan strategy.

e-fundresearch.com: What is the total AUM you manage in all your funds?

Ruth Nash: EUR 238mn (as at 31 October 2012)

e-fundresearch.com: What are the main steps in your investment process?

Ruth Nash: The portfolio is built from the bottom-up and is a collection of our best stock ideas, holding between 40 and 60 stocks. Because the strategy has a lot of stock specific risk, we believe it is important to have exposure to a broad range of sectors.

New investment ideas come from a variety of sources – we follow the daily news flow very closely and often ideas can be generated by an item of news. Broker reports also provide some ideas as do company meetings and announcements. We also run simple, ad hoc screenings looking for criteria which we believe to be important at that point in time, e.g. M&A potential.

Once the initial idea has been generated, the next step is an analysis of 10 years of P&L and balance sheet data. The analysis uses standard ratios but focuses particularly on measures of balance sheet soundness and efficiency and cash flows. Whilst we will take a view on whether company and consensus earnings forecasts are optimistic or conservative, we do not build detailed models to forecast earnings. Instead, we focus on balance sheet analysis, often looking at a company from the perspective of a potential acquirer. Although the past few years have seen a surge in M&A activity in the Japanese market, domestic sell-side analysts tend to ignore takeover potential and focus instead on the immediate earnings outlook when valuing companies. We believe that our approach enables us to uncover value overlooked by the sell-side community.

The next step is to contact the company, either in person, by email, conference call or to ask a local broker to visit on our behalf to answer specific questions which have arisen from the analytical work. With more Japanese companies travelling overseas, corporate access is improving all the time. In 2011, we saw 200 companies in meetings in London and Japan.

e-fundresearch.com: Many Thanks!